by James Corbett

by James Corbett

TheInternationalForecaster.com

August 18, 2015

For those keeping track at home, the Greek farce is finally coming to its foregone conclusion as the country just secured a three-year €86 billion debt slavery bailout deal over the weekend. The first €26 billion will be disbursed Thursday morning, just in time for Greece to fork over its next (odious) debt payment of €3.7bn. All’s well that ends well for the Euro debt monster status quo and the Greek politicians who are happy to sell their population down the river, I suppose. But still . . .

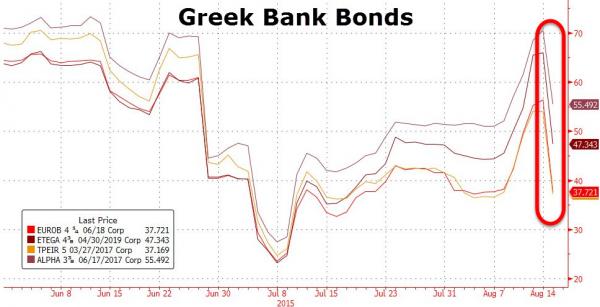

As final details of the package were being released, Eurogroup President Jeroen Dijsselbloem was careful to reassure the markets that there would be no bail-in for bank depositors as the Greek banks–badly depleted from month after month of massive withdrawals–are recapitalized. Then, in the same breath, he caused markets to panic as he announced that senior bank bonds would be bailed in.

“The bail-in instrument will apply for senior bondholders, whereas the bail-in of depositors is explicitly excluded,” he said at a press conference announcing the deal.

The predictable result? Bondholders, blindsided by the news, have panicked and Greek bank bonds have plunged back to pre-bailout levels.

But let’s back up a second. Deposit bail-ins have been excluded? No Cyprus-style bank holidays where depositors’ funds suddenly disappear into the black hole of debt? Surely this is reason for the average Greek to celebrate, right?

Well, maybe not. ZeroHedge is currently reporting that Bloomberg has issued an update to the “no bail-in” promise to add that the promise is only good until January 1, 2016. That’s when new EU-wide legislation designed to harmonize banking regulations across the eurozone goes into effect. The legislation, titled the “Bank Recovery and Resolution Directive (BRRD),” outlines how all member states will be directed as of January 1, 2016, to bring guaranteed deposit levels in line with the new EU-wide standard of 100,000 euros. Essentially this means that from that date forward, any eurozone member’s troubled banks will be susceptible to depositor bail-in for deposits over the 100,000 euro mark.

The problem here is that ZeroHedge does not link to the Bloomberg story in question and if such a caveat exists on the “no depositor bail-in” promise, I haven’t been able to find it. Dijsselbloem has unequivocally stated that depositors are going to be excluded from any potential bail-in and there has been (to the best of my knowledge) no change in this official position. Now of course Dijsselbloem could be (and, given that he’s just another politician, probably is) lying, and, as Olly Burrows of CRT Capital has been quoted as saying, “It is not clear how they will make it possible to bail-in bonds while excluding deposits.” Still, this is the EU we’re talking about, and if the Greek crisis has taught us anything it’s that the banksters can make and unmake the rules whenever they want to suit their whims.

But here’s what we do know for sure: The acceptance of the BRRD was a specific condition of Greece’s bailout package. That’s interesting in and of itself, but in order to see why, we need to know what the BRRD is.

According to the EU itself, the BRRD “provides authorities with more comprehensive and effective arrangements to deal with failing banks at national level, as well as cooperation arrangements to tackle cross-border banking failures,” including (you guessed it) “a comprehensive bail-in tool that ensures that shareholders and creditors bare the cost of bank failure, minimising the burden on taxpayers.” And in the context of failing banks, it should be noted that a bank’s “creditors” include its depositors.

For those who have been following my reporting on the development of the international bail-in regime, you will not be surprised to learn that the EU even boasts that the directive “is fully in line with the Financial Stability Board (FSB) recommendations.” The FSB is a G20-created subsidiary of the Bank for International Settlements, the shadowy bank that Carroll Quigley identified as the “central bank of central banks.” They are currently working quietly behind the scenes to create an international regulatory framework for dealing with banking crises, including the global standardization of the “depositor bail-in” concept we first saw tested in Cyprus two years ago.

For those who have been following my reporting on the development of the international bail-in regime, you will not be surprised to learn that the EU even boasts that the directive “is fully in line with the Financial Stability Board (FSB) recommendations.” The FSB is a G20-created subsidiary of the Bank for International Settlements, the shadowy bank that Carroll Quigley identified as the “central bank of central banks.” They are currently working quietly behind the scenes to create an international regulatory framework for dealing with banking crises, including the global standardization of the “depositor bail-in” concept we first saw tested in Cyprus two years ago.

What? The bailout of Greece was used to put an even tighter globalist bankster regulatory death grip around the Greek people’s throat? Why, I never!

And of course it gets even worse than that. The deal also sets up a new fund dedicated to selling off 50 billion euros worth of government assets and the fire sale has already begun with German-based (of course) FRAPORT already having won the bid to take over operations of 14 regional airports, and deadlines on tenders for the country’s two largest ports and state railways being set for this winter.

Long story short: Yes, Syriza has absolutely sold the Greek people down the river. No surprise there. But should Greek depositors trust Dijsselbloem’s promise that their deposits won’t be touched in the upcoming bank recapitalization? I suppose it depends if you’re the trusting sort. Personally, if I had deposits over 100,000 euros (or really, any deposits at all) in a Greek bank, I’d be doing anything I could to get them out of there.

0 Comments